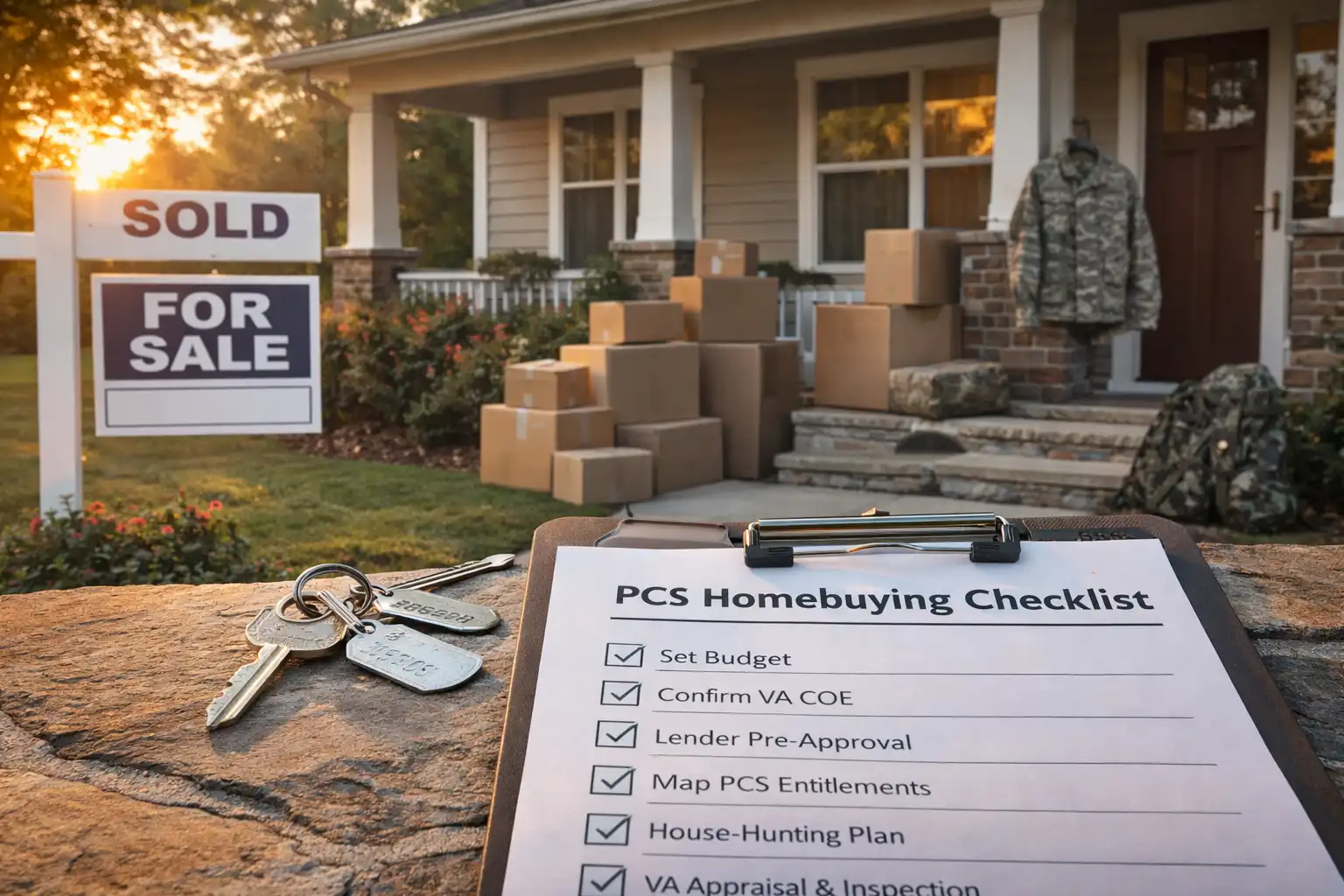

Mission-brief guide for Service Members, Veterans, Guard/Reserve, and spouses.

In short: Buying a home—especially around a PCS (Permanent Change of Station)—is smoother when you prep early. Lock in your budget, confirm your VA Certificate of Eligibility (COE), compare lenders, align your timeline to your report date, and plan for inspections, appraisal, and move logistics. Below is a mission-brief with everything to square away, in order.

1) Set the Mission Parameters (Budget, Timeline, Location)

Define your objective first:

- Tour length & timing: Back-plan from your report date by 60–120 days. That window covers lender pre-approval, house hunting (in-person or virtual), offer, appraisal, and closing buffer.

- Location reality check: Commute gates, traffic patterns, child care/schools, and TRICARE network changes can matter more than square footage. Identify two to three ZIPs you’d live in, not just one.

- Rent vs. buy: If your likely time-on-station is under ~3 years, stress-test the buy scenario (closing costs, potential resale). If >3–5 years, ownership can pencil out more often.

Build your budget:

- BAH (Basic Allowance for Housing): Do not guess. Use the official BAH calculator by ZIP, paygrade, and with/without dependents to anchor your monthly housing envelope.

- All-in monthly: Principal & interest + property taxes + homeowner’s insurance + HOA/condo dues + utilities + maintenance reserve (rule of thumb: 1–2% of home price per year).

- Cash to close: Down payment (if any), closing costs (lender, title, escrow, prepaid taxes/insurance), plus an emergency cushion.

Pro tip: Build two budgets—“house poor” stress test and comfortable. Shop with the comfortable number.

2) Confirm VA Home Loan Readiness

COE (Certificate of Eligibility): This proves to lenders you qualify for VA loan benefits. You can retrieve it yourself online or your lender can usually pull it for you during pre-approval. Start here: How to apply for your COE.

Choose your lender with a VA lens:

- Prioritize lenders who regularly close VA loans near your target installation. Ask how they handle VA appraisal timelines and Minimum Property Requirements (MPRs).

- Request itemized loan estimates (not just payment quotes) so you can compare APR, lender fees, credits, and rate-lock terms apples-to-apples.

- Discuss the VA funding fee & possible exemptions, and how you can finance it or pay it in cash. (No rate quotes here—educational only.)

Pre-approval vs. pre-qualification:

Get underwritten pre-approval if possible. It’s stronger in competitive markets and can accelerate closing.

3) Align Your PCS Entitlements With Your Housing Plan

Know your acronyms—these impact cash flow and timing:

- PCS (Permanent Change of Station): Your official orders drive everything—lender docs, timing, and sometimes occupancy planning.

- HHG (Household Goods) vs. PPM/DITY (Personally Procured Move): Weigh convenience vs. control of delivery timing. Keep certified weight tickets if you do PPM—reimbursements follow the JTR (Joint Travel Regulations) and see MilMove (PPM/DITY).

- DLA (Dislocation Allowance): One-time payment meant to offset move-related expenses (not a house down payment, but it helps cash-flow the transition).

- TLE/TLA (Temporary Lodging Expense/Allowance): TLE (CONUS), TLA (OCONUS)—know what’s reimbursable and for how long.

- POV (Privately Owned Vehicle): Understand whether shipping/storage is authorized (differs CONUS vs. OCONUS). Check USTRANSCOM POV Shipping.

Why it matters for buying:

Entitlements can cover temp lodging while you close, bridge gaps between HHG delivery and move-in, and help you avoid draining your homebuying reserves.

4) Build Your House-Hunting Intel

Must-haves vs. nice-to-haves:

Separate non-negotiables (commute cap, primary bedroom on main level, fenced yard) from wish list (butler’s pantry, three-car garage).

Installation-specific realities:

- Gate access & peak hours: Test-drive (or map) likely routes at “go-to-work/come-home” times.

- Base support & amenities: Think clinics, CDCs/schools, commissary, fitness centers—distance and traffic matter during deployments and shift work.

Virtual-sight-unseen workflow:

If you can’t travel, set standards for video tours (room-by-room, utility panels, attic, crawlspace, street noise), get floor plans and seller disclosures early, and write inspection & appraisal contingencies that reflect you’re remote.

5) Understand VA Appraisal, Inspections & MPRs

Inspection ≠ appraisal:

- Home inspection (optional but strongly recommended): Independent assessment of systems/structure; informs repairs and negotiations.

- VA appraisal (required for VA loans): Confirms value meets the contract price and checks Minimum Property Requirements (MPRs)—health/safety/sanitation (think: adequate heat, roof condition, peeling lead paint mitigation on older homes, proper water/waste systems).

Plan for outcomes:

- If the appraised value comes in low: renegotiate, seller credit, value reconsideration request, or bring difference in cash (discuss with your lender first).

- If MPR repairs are required: Sellers typically complete before closing; build time into your contract and verify completion.

6) Timing the Offer to Your Report Date

Work backward:

- T–120 to T–90 days: Lender shopping, COE, pre-approval, define budget, neighborhoods.

- T–90 to T–60: House hunting (in person or virtual), shortlist, craft offers with protective contingencies.

- T–45 to T–30: Appraisal, inspections, negotiate repairs/credits, rate lock strategy.

- T–21 to T–7: Loan final approval (conditions cleared), insurance binder, utilities scheduled, final HHG plan.

- T–0: Sign, fund, record—keys.

Lease-back or delayed occupancy:

If you arrive before closing or HHG arrives after closing, consider rent-back agreements, short-term lodging, or garage/portable storage to avoid moving twice.

7) Paperwork & Proofs You’ll Need

- Military orders (for PCS) or employment verification

- LES/pay stubs (securely shared—follow lender portal guidance)

- COE (VA)

- Photo ID (government-issued)

- Bank statements (for assets/reserves; again, share securely)

- POA (Power of Attorney) if one spouse/partner will sign alone—coordinate with your lender and title company for VA-compliant POA language

- Insurance quotes (homeowner’s; flood if applicable)

- Earnest money source (paper trail for compliance)

OPSEC/Privacy reminder: Never share SSNs, DoD IDs, medical details, or other sensitive PII outside secure lender/title portals.

8) Craft a Competitive yet Protected Offer

Terms that strengthen your offer (without reckless risk):

- Underwritten pre-approval attached to offer

- Flexible closing date aligned to seller needs (but late enough for your appraisal and HHG plan)

- Reasonable due diligence: Keep inspection contingency; compress timelines only if you can truly execute.

- Appraisal gap language (case-by-case): If used, cap your exposure and confirm cash-on-hand.

Seller credits vs. price:

Don’t be afraid to ask for seller-paid closing costs—sometimes you can increase price modestly to offset the credit and still meet appraisal, depending on comps. Your agent and lender will model the impact.

9) Closing Logistics: Smooth Landing Checklist

7–10 days out:

- Clear-to-close: All loan conditions satisfied

- Final walkthrough: Verify repairs complete; systems operational

- Cash to close: Confirm wire instructions by phone with title/settlement (guard against wire fraud)

- Utilities/Services: Electric, gas, water, trash, internet scheduled for activation on move-in

- Insurance: Policy active on day of closing

Day-of:

Government ID(s), arrange childcare (signing takes time), confirm recording/keys release. If one partner is absent, ensure POA is approved in writing in advance.

10) After Closing: First 30–60 Days

- File homestead or applicable exemptions (varies by state/county).

- Set maintenance rhythm: Replace HVAC filters, test smoke/CO detectors, map water shut-offs, photograph serial numbers for your records.

- Claim mailing address changes (USPS, TRICARE region updates, unit admin/finance updates).

- Document HHG delivery issues swiftly; photos + notations on the inventory form help with claims.

FAQs

Q: Can I buy sight-unseen?

A: Yes, many do around PCS. Protect yourself with strong inspection contingencies, detailed video tours, and reputable local representation.

Q: Can I use BAH to qualify?

A: Lenders typically count BAH as income; they’ll verify via LES and orders. Use the official BAH calculator to frame your budget and talk through ratios with your lender.

Q: What about dual-military or Guard/Reserve status?

A: Loan documentation can vary (e.g., points statements, activation orders). A VA-savvy lender will guide the specifics.

Q: VA loan vs. conventional?

A: VA may offer $0 down potential and no monthly PMI, plus flexible credit parameters and MPR safety standards. Conventional can be competitive if you have larger down payments or specific property types. Compare both with a lender who does a lot of VA business. See the VA loan overview here: VA-Backed Purchase Loan.

Bottom Line

Buying during a PCS goes smoothly when you prep early: set a BAH-anchored budget, secure your VA COE and underwritten pre-approval, map entitlements (DLA, TLE/TLA, HHG/PPM) to your timeline, and plan for inspection/appraisal before you write the offer.

Work with Compass Military

Need a local game plan? The Compass Military Division helps Service Members, Veterans, Guard/Reserve, and military families plan smart housing moves around every PCS. Connect with a Compass Military agent to time your search, closing, and HHG delivery.

Disclaimer

This article is educational, not legal, tax, medical, or financial advice. Policies and local rules vary; confirm details with your lender, title company, and finance office.

Helpful Official Resources

PCS / Entitlements / Regulations

- Joint Travel Regulations (JTR)

- Military OneSource — PCS Hub

- MilMove (PPM/DITY)

- TLA (OCONUS)

- TLE (CONUS)

- POV Shipping (USTRANSCOM)

BAH & Pay

VA Home Loans

- VA Home Loans Hub

- COE — How to Apply

- VA-Backed Purchase Loan

- Funding Fee & Closing Costs

- VA Lender’s Handbook (MPR/Appraisal)

Social Cookies

Social Cookies are used to enable you to share pages and content you find interesting throughout the website through third-party social networking or other websites (including, potentially for advertising purposes related to social networking).